Resource description:

The goal of this report is to review the landscape of current and upcoming ESG market practice around biodiversity (BD) and natural capital in order to inform CircHive data and method needs and steer project development.

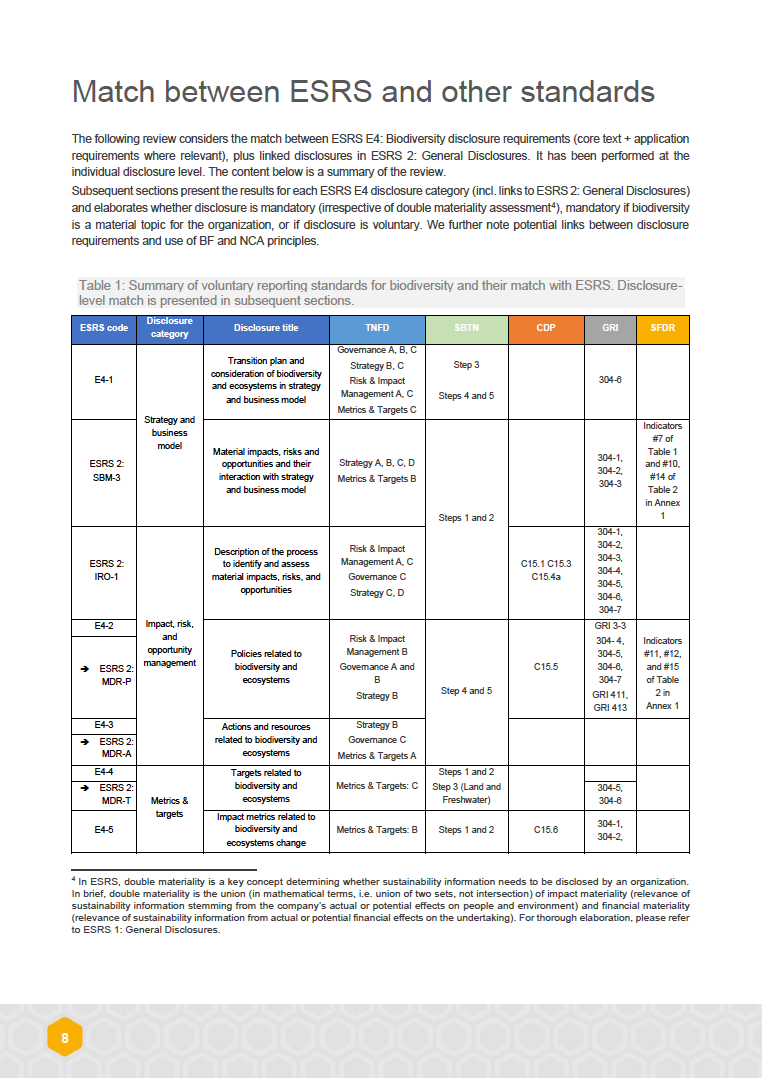

On 5th of January 2023, the EU Corporate Sustainability Reporting Directive (CSRD) entered into force, requiring all large companies and all listed companies (except for micro-enterprises) to disclose information on a range of ESG topics, including biodiversity. Companies subject to CSRD will have to report following the European Sustainability Reporting Standards (ESRS), adopted as of 31st of July 2023. The CSRD aims to ensure that investors and other stakeholders have access to information necessary to assess business impact on people and the environment, and to assess risks and opportunities from ESG issues (including biodiversity). The ESRS do not prescribe specific methodologies for reporting but rather leaves the possibility for companies to use voluntary reporting frameworks to prepare their disclosures (in addition to pointing to certain frameworks in its Application Requirements as a voluntary option). CSRD aims to reduce reporting costs for companies in the medium to long term by harmonizing the ESG-related information that is required.

In the shorter term, a range of mature and newly emerging voluntary reporting frameworks have or are incorporating biodiversity into their disclosure requirements. 2024 is the first year in which companies will need to report under the CSRD1 and there is still no established market practice on the application of the ESRS. Neither is there established practice on the application of voluntary and mandatory reporting standards for biodiversity. This presents a challenge for companies needing to report under the ESRS as they will need to navigate both the new requirements on the CSRD, as well as the new requirements of multiple reporting standards. One of the aims of Task 3.1.1 is to provide guidance on how voluntary and mandatory reporting standards can be used to prepare disclosures under ESRS.

The review is focused on:

- ESRS E4 - Biodiversity

- Linked disclosures from ESRS 2 - General Disclosures on Strategy and Business Models (SBM-3)

- Linked disclosures from ESRS 2 – General Disclosures on Impact, Risk and Opportunity management (IRO-1)

- Linked disclosures from ESRS 2 – General Disclosures Minimum Disclosure Requirements (MDR) for Policies, Actions and Targets (MDR-P, MDR-A, MDR-T)

Author/Contact:

Ivan Paspaldzhiev, denkstatt

Partners:

- Ivan Paspaldzhiev, denkstatt

- Jordan Hairabedian, EcoAct

- Marta Paunova, denkstatt

- Jeanne Barreyre, EcoAct

- Katrin Tomova, denkstatt

Publisher:

Paspaldzhiev, I., Hairabedian, J., Paunova, M., Barreyre, J., Tomova, K. (2023). Review and recommendations for existing and upcoming corporate NC & BD reporting standards.